TV panel price upswing continues in August

Thursday, August 20th, 2020

As TV Panel Prices Skyrocket, 55-inch/32-inch Panel Prices Projected to Rise by 10% in August, Says TrendForce

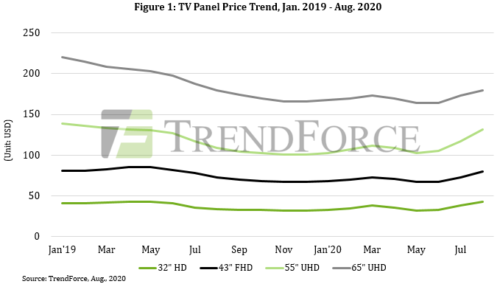

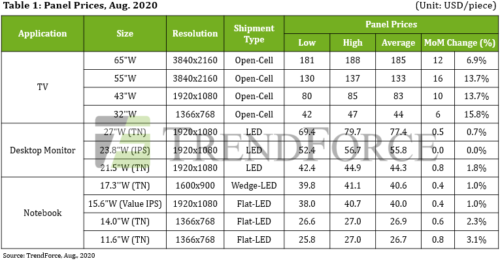

TV panel prices have been maintaining their upswing in August, with 55-inch panels and 32-inch panels each registering price hikes of about 10%, according to TrendForce’s latest investigations. IT panel prices have also been gradually rising, thanks to stable demand from end-markets. Most panel manufacturers are thus expected to make a rebound out of the seven consecutive quarterly losses they had previously suffered and finally turn a profit, in either August or September. As such, the panel industry is projected to make a significant improvement in terms of profitability in 3Q20.

TrendForce Research Vice President Eric Chiou indicates that TV panel quotes are almost entirely dictated by panel manufacturers at the moment. In particular, 55-inch panels and 32-inch panels, which are both made in Gen 8.5 fabs, have been the star performers among various panel sizes by posting the highest price hikes in August. As well, given the strong demand for 43-inch panels, all three panel sizes are projected to register price hikes of about 10% in August. Other panel sizes, namely 50-inch, 65-inch, and 75-inch panels, are expected to record price hikes of 8-10%, 5-7%, and 1-2%, respectively.

TV panel shortage is projected to intensify in 3Q20 as TV brands aggressively stock up in anticipation of capturing TV market share

While the shortage of TV panels has resulted in the recent surge in panel prices in 3Q20, the demand for panels can be attributed to two factors. First, almost all TV brands have been stepping up their panel procurement efforts to prepare for increased retail sales in 2H20; this procurement momentum is projected to last until October. Second, leading TV brands, including Samsung, TCL, and Hisense, have been increasingly favoring the strategy of obtaining competitive advantages by expanding their market shares. This strategy involves a more aggressive shipment of TVs in order to cannibalize competitors’ market shares, further contributing to the overall procurement momentum of TV panels.

With regards to the supply side of the panel industry, because of the consistently high demand for IT panels, manufacturers’ panel capacities have been remaining relatively tight, meaning panel manufacturers may raise TV panel prices as much as possible without worrying about having to digest possible excess capacity. Such a market condition essentially allows manufacturers to raise panel quotes while increasing production levels at an extremely slow and gradual pace. Based on long-term shipment data compiled on TV panels and TV units, TrendForce forecasts an 11% glut ratio between panel suppliers and purchasers in 3Q20, a far lower figure than the average of 20% and also the lowest quarterly glut ratio since the start of 2017. This 11% ratio accurately indicates the fact that panel prices made a rebound from rock bottom due to the overall shortage of panels.

In terms of IT products, monitor panel prices have generally been trending flat or even rising by a small amount. However, high demand in the consumer markets, as well as SDC’s impending exit from the LCD panel manufacturing business at the end of 2020, has resulted in a minor 4-8% rebound for curved monitor open cell quotes in August, the most significant price movement among all monitor product types. On the other hand, NB (notebook computer) panel prices are currently maintaining a slow uptrend of about 1-3% in August thanks to rising demand from WFH and distance education generated by the COVID-19 pandemic.

Latest News

- Netflix posts first quarter 2024 results and outlook

- Graham Media Group selects Bitmovin Playback

- Dialog, Axiata Group, Bharti Airtel agree on merger in Sri Lanka

- Yahoo brings identity solutions to CTV

- Plex has largest FAST line-up with 1,112 channels

- TV3 migrates from on-prem servers to AWS Cloud with Redge