Prices for mid- and large-sized LCD panels keep falling in 3Q

Thursday, July 11th, 2019

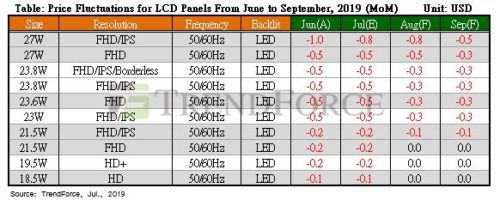

Prices for Mid- and Large-sized LCD Panels Keep Falling in 3Q, Says TrendForce

According to WitsView, a division of TrendForce, prices for mid- and large-sized LCD panels are unlikely to stop falling in 3Q19, mainly due to the trade war that raged on in 2Q. Some LCD brands have already stocked up beforehand as well as raised inventory levels of completed devices in North American regions. Adding the fact that brands are stuck with relatively high inventories of both panels and completed devices as a result of low demand, brands are reducing panel procurement for 3Q, causing restocking momentum to weaken.

“As panel production capacity for 2019 builds up, panel manufacturers are looking to LCD monitor products to help use up the ever growing panel capacity. Among these panels, 23.8-inch sizes have seen a significant increase in supply capacity, but end demand is finding a hard time catching up with that capacity, causing prices for 23.8-inch panels to see a continual descent. As new production capacities continue to appear in 3Q, we forecast that prices for panels of this size may still fall by US$0.3-0.5 MoM under downward pressure,” says TrendForce Senior Research Manager Anita Wang.

27 inches, on the other hand, form the main size of choice for many panel manufacturers and brands, with many high-end devices using panels of this size. Therefore, all products using panels of this size give panel manufacturers a lot of leeway to cut profits. 27-inch IPS panels are forecast to drop by US$0.5-1 MoM in 3Q.

In contrast, prices for small sized TN panels 21.5 inches and below have already neared cash costs, and panel manufacturers aren’t that willing to lower prices any further. Furthermore, 3Q signals the beginning of a peak season for commercial markets in China, bringing 21.5-inch TN panel demand up and presenting the best chance of seeing an end to falling prices.

Latest News

- Barb to start reporting TV-set viewing of YouTube channels

- SAT FILM selects multi-DRM from CryptoGuard

- Qvest and ARABSAT to launch OTT streaming platform

- ArabyAds & LG Ad Solutions partner with TVekstra in Turkey

- Freeview NZ satellite TV service to move to Koreasat 6

- Comscore expands YouTube CTV measurement internationally