Pay TV firms to continue to dominate $126bn US video/TV market

Wednesday, June 21st, 2017Pay TV Firms Will Dominate $126B US Video/TV Market In Spite Of Falling Sales

- Strategy Analytics Reports That OTT Providers like Netflix, Amazon Will Take Less Than 20% of Consumer Spend In 2022

BOSTON, MA — The video and TV market is changing, but not as fast as many people are suggesting. In a new report, Subscription Video and TV Forecast – North America, Strategy Analytics predicts that:

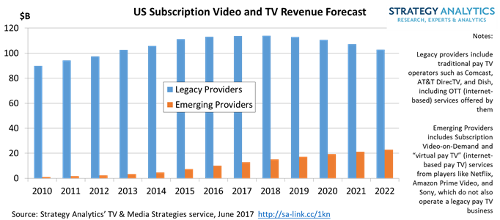

- Overall annual spending on subscription video and TV services in the US will peak at $130.3B in 2019

- Revenues will then decline to $125.7B by 2022

- Established pay TV firms like Comcast and AT&T, including their legacy “managed” pay TV services and new internet-based services like DIRECTV NOW, will still account for more than 80% of total market revenues in 2022

- The share of emerging competitors like Netflix and Amazon will remain below 20% until beyond 2022

- Annual revenue growth for emerging players will fall to just 4.4% by 2022

“It’s not about subscribers, it’s about revenues,” says Michael Goodman, Director, TV & Media Strategies. “Focusing on Netflix subscriber numbers, impressive as they are, ignores the fact that pay TV ARPUs are still more than 10 times higher.”

The report analyzed the convergence of traditional pay TV services offered by firms like Comcast and AT&T with newer subscription video services from Netflix and Amazon Prime Video, as well as internet-based pay TV services like DIRECTV Now, Sling TV, YouTube TV, Hulu Live, and PlayStation Vue. Consumer decision-making and behavior are changing as a result of this evolving marketplace. As a result there are further questions which both traditional pay TV providers and emerging online video players should consider, including:

- To what extent do consumer segments view these services as competing with each other?

- What are the sweet spots that will drive maximum revenues or profitability?

- Which factors drive different consumer segments to choose between the services available?

- How much will consumer segments be prepared to pay for different video content packages?

- How important is the availability of individual content titles, such as TV shows or movies, in affecting choice decisions?

- What is the impact of bundling video with services such as home shopping, mobile or broadband on overall video subscription and usage levels?

The report suggests that video providers will improve their chances of succeeding in this complex new environment if they focus on identifying consumer needs and desired experiences, evaluate their existing products and service offers, and monitor their market performance.

“There is a long way to go before the winners can be announced,” says David Mercer, VP and Principal Analyst. “The long-term transition to IP-delivered video will allow many players to benefit, but understanding consumer needs and how to meet them will be critical to any successful strategy.”

Latest News

- Barb to start reporting TV-set viewing of YouTube channels

- SAT FILM selects multi-DRM from CryptoGuard

- Qvest and ARABSAT to launch OTT streaming platform

- ArabyAds & LG Ad Solutions partner with TVekstra in Turkey

- Freeview NZ satellite TV service to move to Koreasat 6

- Comscore expands YouTube CTV measurement internationally