Global branded TV shipments totaled 219 million units in 2018

Saturday, February 23rd, 2019

TV Brands Seek Differentiation of Specs amid Fierce Competition for Large-Size TVs, Says TrendForce

According to the latest report of WitsView, a division of TrendForce, global shipments of branded TV sets for 2018 totaled 219 million units, an increase of 4.1% compared with prior year, indicating a recovery from weak TV demand in 2017. Looking ahead to 2019, global branded TV shipments are expected to reach 223 million units, an increase of 1.6%

“The year 2018 has witnessed replacement demand in emerging markets such as Latin America driven by the World Cup,” says Jeff Yang, research manager of WitsView. The steady economy situation in North America was also favorable for the recovery of global TV demand. TV brands were willing to offer promotions as well, considering the downward trends in overall TV panel prices last year.

The supply of large-size panel will increase greatly in 2019 with new production capacity. CSOT’s Gen 11 fab, HKC’s Gen 8.6 fab, and Sharp’s Gen 10.5 fab in Guangzhou are expected to enter the market at the beginning, middle, and end of the year respectively. Decreasing panel prices will bring unavoidable pressure on the suppliers, but will also make large-size TVs cheaper. In the future, the TV industry will bound to seek constant improvements in specs to create brand value and differentiate their products.

TV brands accelerate their layout for large-size TVs

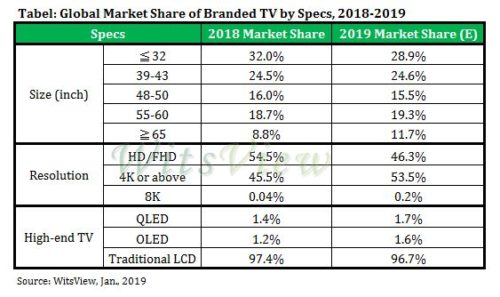

For TV brands, there is little room for product differentiation for TV smaller than 32 inches, because most of them are positioned as entry-level products, and the costs of panels are relatively transparent due to long-term oversupply of panels under 32 inches. Therefore, TV brands have been decreasing the portion of 32-inch TVs or smaller ones in their product mixes, and the percentage is expected to be less than 30% in 2019.

On the other hand, the portion of 55-inch TVs or larger ones is increasing. The percentage of 65-inch TVs or above is expected to increase from 8.8% in 2018 to 11.7% in 2019. As for the retailing prices of TVs in the North American market last year, 65-inch TVs were priced between $399 and $699, while 75-inch ones were mostly priced above $1,500. With the falling prices of large-size TVs, there is a chance to see ultra-low-priced 75-inch TV below $799 in the peak season promotion during the second half of this year.

QLED TVs face more competition from large-size LCD and OLED counterparts

The price decline of large-size panels will drive more TV brands into the large-size TV segment. However, in the future, large-size TVs will not necessarily be a guarantee of profits. For first-tier brands, the development of large-size TV business will be even more difficult. On the other hand, the sales of QLED TVs, which have more price advantages, is no worse than OLED TV. The high-end 55/65-inch QLED TVs from Samsung were priced at about US$1,000 to US$1,500 during the year-end promotion, while the prices of 55/65-inch OLED TVs remained above $1,500.

However, the prices of OLED panels are expected to decrease in 2H19, because the long-term undersupply of OLED panel would be slightly eased considering LGD’s planned investment in its Guangzhou OLED fab in the second half of this year. In addition, there is pressure from low-cost 75-inch LCD TVs. For the two reasons, it remains to be seen whether Samsung is able to maintain price advantage of its QLED TV this year.

TV brands move toward 8K, HDR, and borderless products for differentiation

The market of 4K TV has matured, with the share of 4K products expected to exceed 50% in the TV market in 2019. As for 8K TV, the content, transmission, hardware, as well as the whole industry chain have not been well developed. The prices of 8K panels are still more than twice the prices of 4K ones. Therefore, it remains to be seen whether 8K TV can copy the development mode of 4K TV. WitsView estimates that 8K TVs would account for only about 0.2% of the total TV shipments this year.

Compared with the upgrade to 8K TV, it is relatively easier to increase the added value of products by differentiating the specs, such as the Mini LED and dual cell design, which can achieve a high dynamic contrast (HDR), and the design of a full-screen without borders. These are all the potential specs upgrade that TV brands can consider.

Latest News

- Barb to start reporting TV-set viewing of YouTube channels

- SAT FILM selects multi-DRM from CryptoGuard

- Qvest and ARABSAT to launch OTT streaming platform

- ArabyAds & LG Ad Solutions partner with TVekstra in Turkey

- Freeview NZ satellite TV service to move to Koreasat 6

- Comscore expands YouTube CTV measurement internationally