Pandemic-induced decline in display driver IC demand temporarily alleviates tight supply

Monday, April 13th, 2020

Pandemic-Induced Decline in Large-Size DDI Demand Temporarily Halts Tight Supply Issues, which May Resurface in 2H20, Says TrendForce

According to the latest investigations by the WitsView research division of TrendForce, disappointing 1Q20 shipment performances by panel manufacturers, combined with the continued acceleration of the COVID-19 pandemic in Europe and the U.S., resulted in a reduction of proposed TV panel purchases in 2Q20 by several major TV brands. Despite urgent orders for IT panels due to the increased need for telework, overall IT panel demand following the fulfillment of these urgent orders remains yet unclear. As such, the previous projection of tight large-size DDI supply in 2020 has not surfaced at the moment.

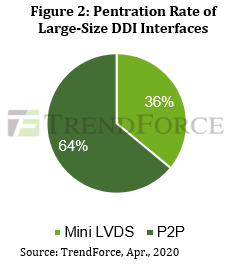

In general, there are two types of interfaces connecting large-size DDI and display panels, according to TrendForce: mini LVDS and high speed P2P. TrendForce estimates yearly demand for DDI with mini LVDS interface from three major applications, namely, notebook, monitor, and TV panels, to be about 1.5 billion units, with monthly wafer demand reaching 50-60 KSH (k sheets). UMC, TSMC, and VIS, foundries which supply DDI, favor orders for DDI with P2P interfaces and intend on fulfilling P2P orders instead of mini LVDS in the future because of higher profit margins. These companies have instructed IC design houses to redirect mini LVDS manufacturing orders to other foundries.

PSMC and Nexchip, foundries that are the most likely to increase wafer inputs for mini LVDS, do not currently have enough production capacity to meet the overall industrial demand for the interface. Conversely, demand for PMIC and entry-level and mid-range CMOS sensors has not cooled down. Forehead thermometer microcontroller units have also been in short supply since the inception of the COVID-19 pandemic. As such, major foundries’ 8-inch wafer inputs have been seeing near-maximum utilization rates. If the pandemic can be effectively contained, demand for DDI interfaces from major end-device applications is expected to resurface in 2H20, in turn resulting in a tight supply of large-size DDI once again.

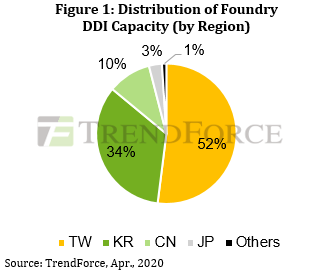

Analysis of total foundry wafer inputs for DDI applications shows an average of 250-270 KSH per month for 8-inch wafer inputs and 120-150 KSH per month for 12-inch wafer inputs in 2019. When converted into equivalent 8-inch wafer inputs by size, total wafer inputs (8-inch and 12-inch combined) for DDI applications reached 550-600 KSH per month. Ranked by total production capacity, Taiwan leads other regions by accounting for more than 50% of wafer inputs for DDI applications, with South Korea following behind at 34%, and China, Japan, and other regions trailing at 10%, 3%, and 1%, respectively.

In terms of DDI wafer input by foundry, UMC is the leading supplier, with Samsung LSI and SK Hynix ranked second and third. As leading supplier UMC takes a large number of orders from IC design houses in Greater China, if the foundry were to reallocate its wafer capacity for various applications, there will be a corresponding panic on the market regarding potential issues regarding DDI supply. Conversely, as the Korean supply chain is more closed-off in comparison, there are fewer Greater China-based IC design houses placing orders for wafer input at Korean foundries. Thus, Samsung LSI and SK Hynix do not influence the DDI market’s overall supply and demand as much as UMC does.

Latest News

- Barb to start reporting TV-set viewing of YouTube channels

- SAT FILM selects multi-DRM from CryptoGuard

- Qvest and ARABSAT to launch OTT streaming platform

- ArabyAds & LG Ad Solutions partner with TVekstra in Turkey

- Freeview NZ satellite TV service to move to Koreasat 6

- Comscore expands YouTube CTV measurement internationally