TV panel shipments decreased 3.5% M-o-M in February

Tuesday, March 24th, 2020

Under COVID-19 Pandemic’s Influence, February LCD TV Panel Shipment Declined by 10.2% Compared to Previous Shipment Target, Says TrendForce

According to the latest investigations by the WitsView research division of TrendForce, despite the impact from the COVID-19 pandemic, February TV panel shipments were propped up by rising panel ASPs and panel manufacturers’ existing stock. Monthly TV panel shipment decreased by 3.5% MoM in February, reaching 20.073 million units. This figure is a 10.2% decline from the shipment target set in 2019 but remains higher than previously projected decline of 18%.

Although TrendForce expects TV panel shipment in March to fall below the target set in 2019 by 6.1%, the pandemic’s effect on labor, logistics, and material supply remains a gradual process, meaning panel shipment in March may yet surpass February figures by about 14%, for a total of 22.9 million units.

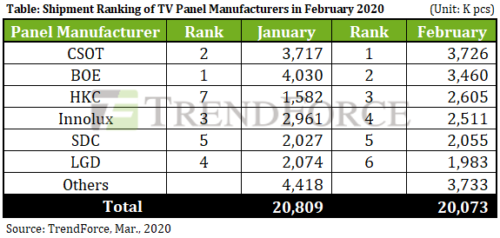

As TV panel shipment ranking saw a major reshuffle, CSOT led the pack for the first time

In terms of the top six panel manufacturer’s performances, CSOT was the first to resume operations and maintained a healthy component inventory level. Not only did the company suffer the least damage from the pandemic, but it also took advantage of the twin surges in panel price and demand by aggressively escalating its shipment. CSOT registered February shipment of 3.726 million units, a 0.2% MoM increase, and gained pole position for the first time by overtaking BOE.

Although second-ranked BOE, which manufactures multiple product lines, obtained a special government permit to bypass lockdown and stay open after the outbreak, the company operated various fabs located throughout China; the scattered nature of these facilities meant BOE was more affected by the labor shortage issues than other panel manufacturers were. As well, BOE suffered from the shortage of upstream components, such as polarizing films and PCBs. All of the aforementioned factors resulted in an MoM reduction of 14.1% in BOE’s February shipment, which registered 3.46 million units, the company’s worst performance since June 2017.

Despite issues with material shortage, HKC fulfilled its deferred January shipment in February, in turn scoring a considerable MoM increase of 64.7% by shipping 2.605 million units. The company leapfrogged to reach third place in monthly shipment performance and became the dark horse of the month.

In addition to delayed work resumption at its back-end IC bonding fab, fourth-ranked Innolux also faced labor and material shortages, leading to a massive 15.2% MoM shipment decline, down to 2.511 million units.

In comparison, Korean panel manufacturers suffered relatively limited losses from the pandemic. Despite temporary labor shortages at its Suzhou-based IC bonding fab in February, fifth-ranked SDC was able to increase the capacity utilization rate of its Korean fabs due to panel price hikes in early 2020. SDC shipped 2.055 million panels in February, a 1.4% MoM increase. LGD did not face major shortages in raw materials, but owing to the fewer available workdays in February and the impact on shipment performance from the company’s decision in 2H19 to slash its Korean fabs’ LCD TV production capacity, LGD posted a MoM shipment decrease of 4.4% in February, shipping 1.983 million units and ranking sixth on the list, while setting a historical low in single-month shipment.

TV panel shipment in 1Q20 is projected to be 5.6% lower than shipment target set in 2019

Given poor fulfilment rates in February and March, TrendForce projects a cutback in 1Q20 TV panel shipment, down to 63.782 million units, a 12.7% QoQ and 8.9% YoY drop. This figure is 5.6% lower than last year’s shipment target for 1Q20. On the other hand, the sudden reduction in panel supply galvanized a higher-than-expected rise in 1Q20 TV panel ASP.

In 2Q20, as panel demand becomes partially deferred, and manufacturers skyrocket panel shipments in a bid to destock their front-end liquid crystal cells, TV panel shipment is expected to potentially increase by 7.1% QoQ. However, the global pandemic will take a heavy toll on the overall economy, with rising unemployment and plummeting global GDP in turn diminishing consumers’ purchasing power. As the upstream/downstream panel supply chain gradually makes a full recovery, the industry is expected to once again face the issue of supply and demand.

Latest News

- Barb to start reporting TV-set viewing of YouTube channels

- SAT FILM selects multi-DRM from CryptoGuard

- Qvest and ARABSAT to launch OTT streaming platform

- ArabyAds & LG Ad Solutions partner with TVekstra in Turkey

- Freeview NZ satellite TV service to move to Koreasat 6

- Comscore expands YouTube CTV measurement internationally