Streaming consumers desire simplicity in entertainment experiences

Wednesday, December 21st, 2022

Six in Seven Consumers Desire Simplicity in Entertainment Experiences, Accenture Report Finds

- “Reinvent for Growth” report highlights how media companies can improve user experiences and drive revenue with new entertainment ecosystems

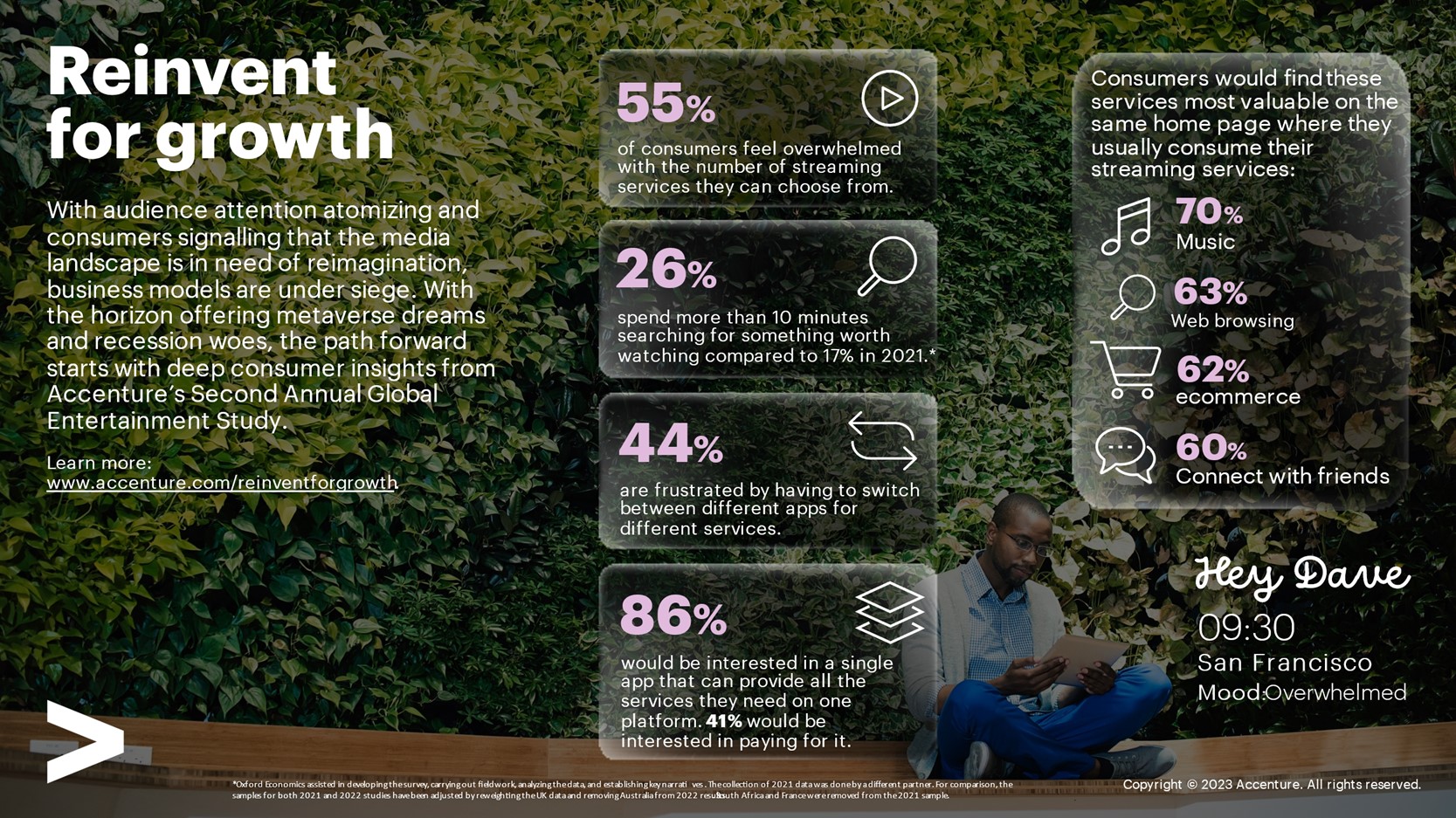

NEW YORK — Six in seven consumers globally (86%) want an all-in-one platform to simplify their entertainment experiences with video streaming, fantasy sports, social media, ecommerce and more, according to “Reinvent for growth,” a new report from Accenture (NYSE: ACN).

As part of its second annual global entertainment study, Accenture surveyed 6,000 consumers to understand their preferences and behaviors regarding their online entertainment experiences. Four in 10 respondents (41%) said they would pay for an all-in-one platform for their entertainment services. In addition, three in five (61%) want the ability to share their streaming profiles across platforms to allow for better personalization of content.

“Standalone streaming services are running up against some simple facts: There are limits to what consumers will pay for and only a certain amount of complexity and options that they are prepared to deal with,” said John Peters, a managing director in Accenture’s Media & Entertainment industry practice. “It is time to reimagine entertainment ecosystems so that media companies can move to profitable growth by helping consumers get everything they need and want.”

Other findings from the report further highlight the need for media organizations to reconsider their operational and content strategies:

- More than one-third (35%) of consumers unsubscribed from at least one of the top five streaming video-on-demand services in the last 12 months, and 26% said that they plan to cut one or more in the next 12 months.

- More than seven in 10 consumers (72%) reported frustration at finding something to watch, up 6 percentage points from last year.

- More than half (55%) of consumers said they are overwhelmed by the number of streaming services to choose from, with 26% saying it can take them more than 10 minutes to settle on a streaming choice (up from 17% last year).

Accenture’s report also identifies three emerging roles for entertainment companies that are competing for consumers’ time, attention and money:

- Audience aggregators are platform companies with a diversified business model that monetize attention and engagement directly and indirectly by tying multiple entertainment and other services together in one place.

- Audience cultivators will create and efficiently monetize entertainment in one or multiple forms (e.g., video, music, gaming etc.) by knowing their core audience, focusing on content/cost efficiency, and ensuring that they’re included in audience aggregator platforms and bundles.

- Content merchants will focus on making the best possible content without needing to monetize the engagement their content achieves.

“The future of the media industry is moving toward aggregated platforms,” said Imran Shah, a managing director with Accenture’s Communications, Media & Technology industry group. “These platforms will achieve two crucial outcomes — creating inclusive, lower churn services and bundles that will drive revenue for media companies, while delivering experiences that enable consumers to easily find and access content.”

Research Methodology

Accenture conducted research to gain an understanding of consumers’ preferences, beliefs and behaviors on their online entertainment experiences. The online survey of 6,000 consumers aged 18+ in 10 countries (Australia, Brazil, Canada, Germany, India, Italy, Japan, Spain, the U.K. and the U.S.) was designed to identify significant changes to the existing direct-to-consumer media regime and offer suggestions for brands across the media spectrum to adapt their model to be more relevant and successful with customers. Fieldwork was conducted between October and November 2022.

Oxford Economics assisted in developing the survey, carrying out fieldwork, analyzing the data, and establishing key narratives. The collection of 2021 data was done by a different partner. To ensure appropriate comparisons, the samples for both 2021 and 2022 studies have been adjusted to have a similar structure.

Latest News

- Barb to start reporting TV-set viewing of YouTube channels

- SAT FILM selects multi-DRM from CryptoGuard

- Qvest and ARABSAT to launch OTT streaming platform

- ArabyAds & LG Ad Solutions partner with TVekstra in Turkey

- Freeview NZ satellite TV service to move to Koreasat 6

- Comscore expands YouTube CTV measurement internationally