Telecom and pay-TV revenue in New Zealand to remain stagnant

Monday, January 29th, 2024

Telecom and pay-TV services revenue in New Zealand to remain stagnant with 0.7% CAGR over 2023-28, forecasts GlobalData

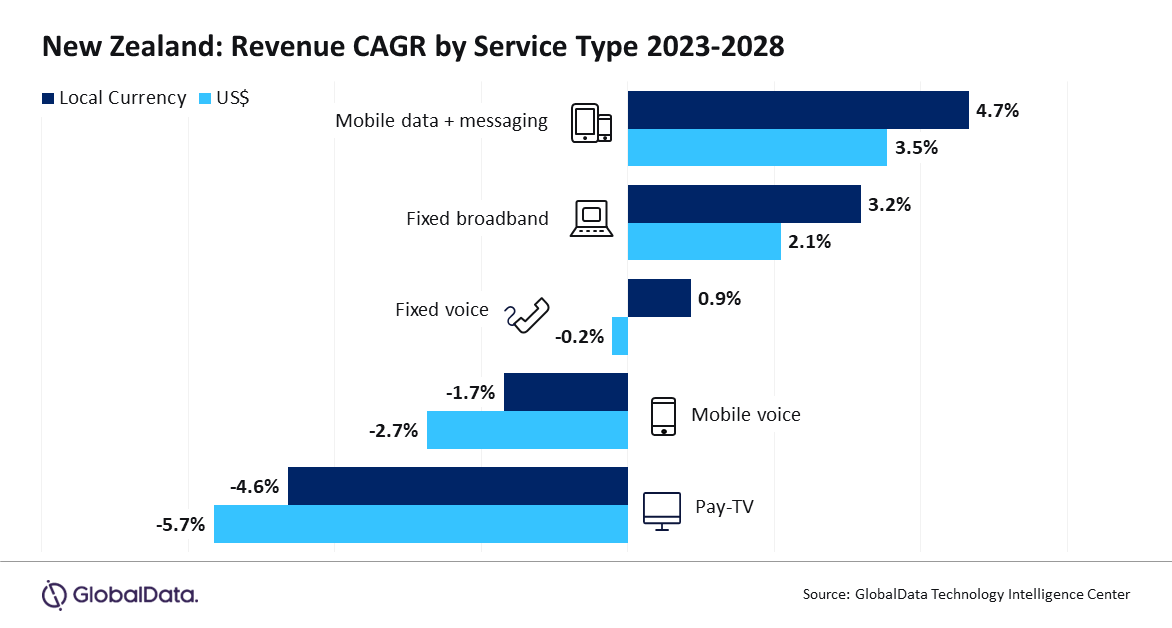

The total telecom and pay-TV services revenue in New Zealand is poised to register a marginal compound annual growth rate (CAGR) of 0.7% between 2023 and 2028, with continued decline in mobile voice service revenue denting the overall growth prospects, despite considerable revenue growth in mobile data and fixed broadband segments, according to GlobalData, a leading data and analytics company.

GlobalData’s New Zealand Telecom Operators Country Intelligence Report reveals that the mobile voice service revenue in the country is set to decline at -2.7% CAGR over the forecast period in line with the steady decline in mobile voice service ARPUs, as customers increasingly adopt internet-based communications and operators bundling free voice minutes with their unlimited plans.

Mobile data service revenue on the other hand will increase at a CAGR of 4.2% over the forecast period, which will be driven by the continued rise in mobile internet subscriptions, and growing adoption of higher-ARPU yielding 5G services.

Aasif Iqbal, Telecom Analyst at GlobalData, comments: “4G services accounted for the largest share of the total mobile subscriptions in New Zealand in 2023. However, the share of 4G subscriptions will decline drastically during the forecast period, owing to the migration of subscribers from 4G to 5G networks”.

“5G’s share will increase rapidly to reach 32.2% in 2028, thanks to the widespread availability of 5G services in the country, made possible by telcos’ focus on 5G network expansions and service improvements. Spark New Zealand, for instance, aimed to expand its 5G network coverage across 90% of the country’s population by 2023.”

In the fixed communication services segment, fixed broadband service revenue will increase at a CAGR of 2.1% during 2023-2028 period, driven by growth in the FTTH and fixed wireless subscriptions on the back of efforts by the government and operators to further expand broadband connectivity in the country. Fixed voice service revenue, on the other hand, will decline marginally during the forecast period.

Iqbal adds: “The growing demand for higher-speed broadband connectivity and the availability of FTTH services across the country will support the growth of fiber broadband service adoption over the forecast period. For example, Chorus, a wholesale fixed line provider, has deployed 1,031,000 fiber lines in 2023, up from 959,000. Chorus is also planning to retire its copper network by 2033 and become an all-fiber company.

Pay-TV services revenues in the New Zealand will decline at a negative CAGR of 5.7% during the 2023-2028 period, in line with the continued drop in DTH subscriptions, increasing consumer shift to OTT video platforms such as Netflix, and the subsequent decline in pay-TV ARPU levels.

Iqbal concludes: “One New Zealand (Formerly Vodafone New Zealand) led mobile services market in 2023 in terms of subscriptions and will continue to hold the top position through the forecast period, supported by its strong focus on mobile network developments. The operator is also focusing on M2M/IoT opportunities with plans to cover up to 60% of the geographic area with NB-IoT network by 2024.”

Spark New Zealand led the fixed broadband services market and will retain its leadership through 2028, supported by its strong footprint in the FTTH segment.

Sky, which operates in the DTH segment, is the only player operating in the pay-TV services market. The operator continues to offer a variety of pay-TV packages that cater to diverse subscriber demands, including kids and family content, entertainment, sports, movies.

Links: GlobalData

Latest News

- Barb to start reporting TV-set viewing of YouTube channels

- SAT FILM selects multi-DRM from CryptoGuard

- Qvest and ARABSAT to launch OTT streaming platform

- ArabyAds & LG Ad Solutions partner with TVekstra in Turkey

- Freeview NZ satellite TV service to move to Koreasat 6

- Comscore expands YouTube CTV measurement internationally