China TV brands shrug off headwinds in 1Q, says WitsView

Monday, May 27th, 2019

China TV Brands Fear Not the Developing Dispute, Shrugging Off Headwinds in Shipments 1Q, Says TrendForce

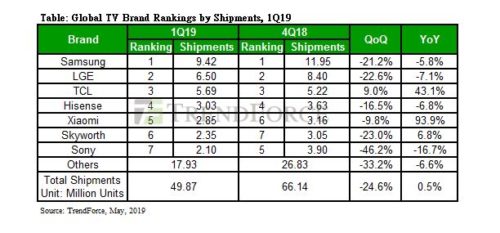

WitsView, a division of TrendForce, has it in its latest report that shipments of TV brands worldwide came to 49.87 million units for 1Q19, a QoQ slide of 24.6% and a YoY bump of 0.5%. One may discover from the brand shipment rankings that first and second place are still the domain of Korean brands, while China brands fill up third to sixth, evidently proving themselves a force to be reckoned with in their ambitions to aggressively raise market share by leveraging their cost advantage.

“Entering the second quarter, small-sized TV panel prices struggle to make a comeback in May due to the lack of improvement in end demand, with TV brand inventory strategies predicted to turn conservative in 2Q and overall shipments possibly to exhibit a 1~1.5 % QoQ decline,” says TrendForce Research Manager Jeff Yang. Besides observing whether China’s 618 sales event may successfully move consumers to spend their money, it is also worth paying attention to the Chinese brands keen on expanding territory in the US market, such as TCL and Hisense. These companies will be heavily hit by the US-China trade dispute, should the wildfire spread to TV products.

For TCL, its maximum Mexican production capacity can barely meet half of North America’s demand for TCL’s TVs. Faced with the US’s 25% tariff imposed on China, they are forced to ramp up Mexican capacity, This also means that the age-old strategy of Chinese brands to drive sales through price leveraging will be met with resistance.

Korean Brands Focus Development on High-End Products, with TCL Closely Following LGE in Shipments

Pressured by creeping China brands and diminishing profits in the TV industry, the two Korean brands are each hoping to secure a competitive edge and raise profitability with the help of high-end products. Samsung is resorting to raising the specs of its 8K+QLED TVs , while LGE is focusing on expanding its OLED TV markets. A profit-oriented strategy, however, will also impact shipments. Although Samsung held steady at first place with 9.42 million in shipments in 1Q, its QoQ and YoY declines came to 21.2% and 5.8%, respectively. LGE’s 1Q shipments also fell by 22.6% QoQ and 7.1% YoY.

TCL already stood steady at third place in annual shipments for 2018, with 1Q shipments having reached 5.69 million units in the first quarter this year, narrowing its distance with LGE to under 1 million units. TCL has already come in possession of CSOT’s panel resources, and has even announced plans to make a splash with investments into TV module production in India, demonstrating its ambitions to expand its worldwide market.

Hisense and Skyworth Raise Sales in Targeting Markets Overseas, While Xiaomi Finds its Way to No. 5

China’s traditional TV brands, Hisense and Skyworth, reached 3.03 million and 2.35 million in shipments 1Q, standing at fourth and sixth place, respectively. After last year, which saw Hisense open sales of OLED TVs in Australia, Hisense will be moving into China OLED TV territory this year. Skyworth, on the other hand, has been and still is LGD OLED’s long-term strategic partner. In stalling-demand China, OLED TVs have become important products of Hisense’s and Skyworth’s in their efforts to raise brand strength. As for sales growth, Hisense and Skyworth have placed their hopes on markets overseas, aiming to raise the proportion of sales overseas by leveraging their low-cost advantage.

Xiaomi’s 1Q shipments came to 2.85 million units, reaching 93.9% in YoY growth and securing fifth place. As traditional China TV brands lower costs by deepening supply chain integration, Xiaomi took a different approach, adopting a business model that focuses solely on product development, sales channels and Xiaomi’s fan base, while production is outsourced to ODMs in order to alleviate operational and production costs. Although Xiaomi has successfully developed a new business model by utilizing the IoT ecosystem, TCL was Xiaomi’s main ODM last year, while this year sees Xiaomi strengthening its collaboration with another ODM: BOEVT. From this, it is clear that cost management along the panel supply chain still forms the key to success for TV brands.

Latest News

- Barb to start reporting TV-set viewing of YouTube channels

- SAT FILM selects multi-DRM from CryptoGuard

- Qvest and ARABSAT to launch OTT streaming platform

- ArabyAds & LG Ad Solutions partner with TVekstra in Turkey

- Freeview NZ satellite TV service to move to Koreasat 6

- Comscore expands YouTube CTV measurement internationally