2020 U.S. multichannel video loss tops 7 million

Monday, March 8th, 2021

2020 U.S. multichannel video loss tops 7 million, virtual subscription momentum slows in Q4

NEW YORK — Traditional U.S. multichannel plumbed new depths in 2020 with a decline of nearly 7.2 million subscriptions, according to full market estimates from Kagan, a media research group within S&P Global Market Intelligence.

Virtual multichannel services blunted the overall erosion of people taking a package of live linear channels, but the estimated 2.7 million new subscribers for the services that increasingly resemble the traditional services being displaced fell short of offsetting cable, telco and satellite defections.

Losses for those traditional cable, telco and satellite providers slowed in the fourth quarter but the full-year decline underscored that the impacts of the pandemic amplified cord cutting instead of insulating an industry built around home entertainment.

The fourth quarter offered an overall improvement in traditional subscription losses at 1.5 million, but the virtual segment did not maintain the surprising momentum from the third quarter, tallying a tepid estimated gain of 223,000 to finish the year at nearly 12.5 million subscriptions.

“Americans continue to leave traditional video services in droves, with 6.8 million households cutting the cord in 2020,” said Tony Lenoir, senior analyst with Kagan.

Additional penetration takeaways from Kagan’s full year 2020 report:

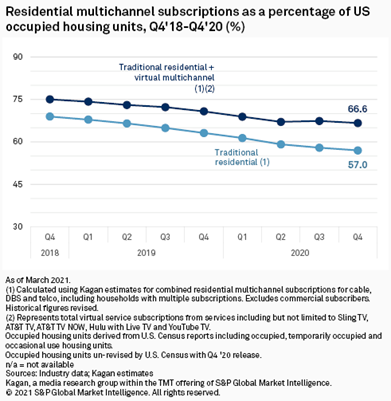

- The combined penetration of traditional and virtual subscriptions, which accounts for the total households in the U.S. taking a package of live, linear channels, dropped below 67% at year end.

- The percentage of households in the U.S. with a traditional multichannel subscription dropped to less than 57%.

S&P Global Market Intelligence’s Kagan research team provides in-depth coverage and deep analyses of the global technology, media and telecommunications sectors (TMT). This TMT research offering complements S&P Global Market Intelligence’s broad universe of research sector coverage including energy, enterprise technology, financial institutions groups, leveraged loans, and metals & mining.

S&P Global Market Intelligence’s opinions, quotes, and credit-related and other analyses are statements of opinion as of the date they are expressed and not statements of fact or recommendation to purchase, hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security.

Latest News

- Barb to start reporting TV-set viewing of YouTube channels

- SAT FILM selects multi-DRM from CryptoGuard

- Qvest and ARABSAT to launch OTT streaming platform

- ArabyAds & LG Ad Solutions partner with TVekstra in Turkey

- Freeview NZ satellite TV service to move to Koreasat 6

- Comscore expands YouTube CTV measurement internationally