Inflation driving telecommunication services revenue growth

Friday, November 3rd, 2023

Global Market for Telecommunications Services Has Accelerated Again, Fueled by Inflation, But Not in All Regions, According to IDC

NEEDHAM, Mass. — Worldwide spending on telecommunication and pay TV services will reach $1.55 trillion in 2023, an increase of 3.0% over 2022, according to the International Data Corporation (IDC) Worldwide Semiannual Telecom Services Tracker. The latest forecast is one percentage point higher than the previous forecast, published in May. This is the third increase in the forecast in the last 12 months, with inflation being the primary driver.

The geographic regions seeing above-average forecast revisions are the Middle East and Africa (MEA) and Latin America. This is mainly a consequence of hyperinflation happening in countries such as Turkey, Uganda, Egypt, and Argentina, where it has become normal to see quarterly ARPUs (average revenue per user) growing by more than 50% on a yearly basis. On the other hand, expectations for the telecom services market in Western Europe have been lowered slightly primarily due to a worsened economic environment in a few key countries, including Germany. IDC believes this is the first sign of a new market force emerging that will put the current growth rates under pressure and slowly bring them down toward the end of the forecast period.

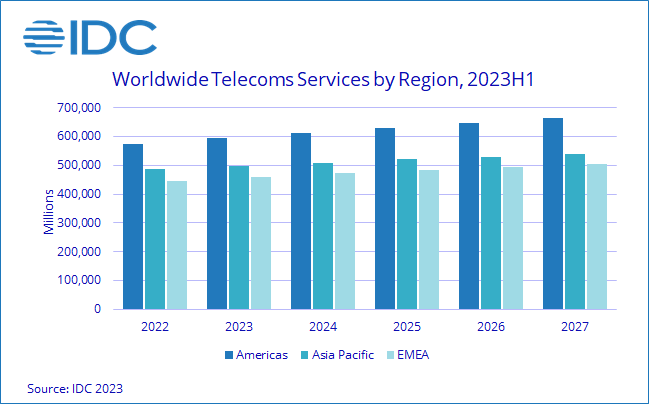

Regional Telecom Services Revenue and Year-on-Year Growth (revenues in $US billions)

Global Region 2022 Revenue 2023 Revenue 2023/2022 Growth ------------- ------------ ------------ ---------------- Americas $575 $594 3.3% Asia/Pacific $486 $499 2.6% EMEA $447 $461 3.1% ------------- ------------ ------------ ---------------- Grand Total $1,509 $1,554 3.0%

Source: IDC Worldwide Semiannual Services Tracker – 1H 2023

Inflation is certainly a global phenomenon, but the trends it shapes in different local markets vary significantly. In many countries, telecom operators were allowed by regulators to increase their tariffs (often applying a Consumer Price Index model), resulting in healthy service revenue growth on an annual basis. In other countries, however, this move drove the accelerated migration of customers to cheaper tariff packages and cheaper operators, so the value growth rates were much lower than the nominal tariff increases. A third group includes countries such as Italy, where the competitive situation did not permit operators to do any tariff adjustments. And among a fourth group of countries, mainly the developing countries in Eastern Europe and Africa, tariff increases were prevented by the populations’ low purchasing power.

An analysis by type of telecom services confirms that the well-known trends continue despite the changes in top-line forecasts. Mobile is and will remain the largest segment driven by the growth in mobile data usage and machine-to-machine (M2M) applications, which are offsetting declines in spending on mobile voice and messaging services. The fixed data services segment will also grow driven by the need for higher bandwidth services. Spending on fixed voice services will fall over the forecast period as rapidly declining TDM voice revenues are not being offset by the increase in IP voice. The traditional Pay TV market will decline slightly over the forecast period due to the growing popularity of video on demand (VoD) and over the top (OTT) services, but these services will remain an important part of the multi-play offerings of telecom providers across the world.

Prices of all goods and services have been increasing for quite some time. Economic growth has recently started to decelerate following increases in Central Bank interest rates. Consumers and businesses have been under pressure as they try to maintain a balance between rising costs and limited budgets. Although the elasticity of the telecom services is relatively low, and it is hard for customers to imagine everyday life without them, any excessive tariff increases might affect demand.

“Operators need to carefully evaluate every single market for tolerance to price increases,” said Kresimir Alic, research director, Worldwide Telecom Services at IDC. “They should continuously assess and compare the product mixes, quality of services, pricing, and customer support capabilities of all supply-side participants. That information should help them find a magic percentage that will not scare the customers away, have positive impact on revenues, and help them maintain healthy margins in these turbulent times.”

Links: IDC

Latest News

- Barb to start reporting TV-set viewing of YouTube channels

- SAT FILM selects multi-DRM from CryptoGuard

- Qvest and ARABSAT to launch OTT streaming platform

- ArabyAds & LG Ad Solutions partner with TVekstra in Turkey

- Freeview NZ satellite TV service to move to Koreasat 6

- Comscore expands YouTube CTV measurement internationally