NAGRA claims top spot in Conditional Access market

Wednesday, September 13th, 2017

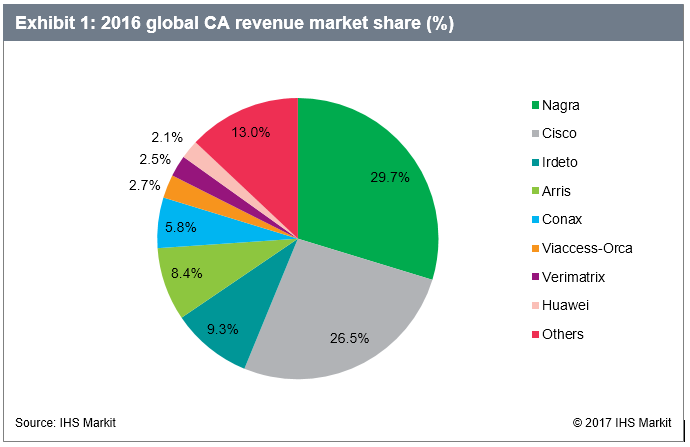

LONDON — 2016 was a pivotal year for the content security industry. While global Conditional Access (CA) spend fell imperceptibly – from $1.97 billion to $1.92 billion – the market’s most volatile change took the form of competitive re-alignment. Cisco’s CA revenue contracted by 17 percent, the firm retreated from its dominant market position and NAGRA absorbed the vast majority of Cisco’s relinquished turnover. In so doing, NAGRA vaulted into the CA market’s top spot, and now controls 30 percent of CA spend. In conjunction with Conax, another Kudelski Group security provide, the combined group entity controls 35 percent of the global CA market and leads the industry by a considerable margin.

“The content security industry is rife with competitive repositioning and strategic maneuvering,” said Merrick Kingston, principal analyst at IHS Markit. “Ultimately, however, NAGRA’s advance is attributable to a single empirical antecedent: the firm has shown unparalleled commitment to broadening the scope and capability of its security portfolio.”

Capabilities vary in the security segment

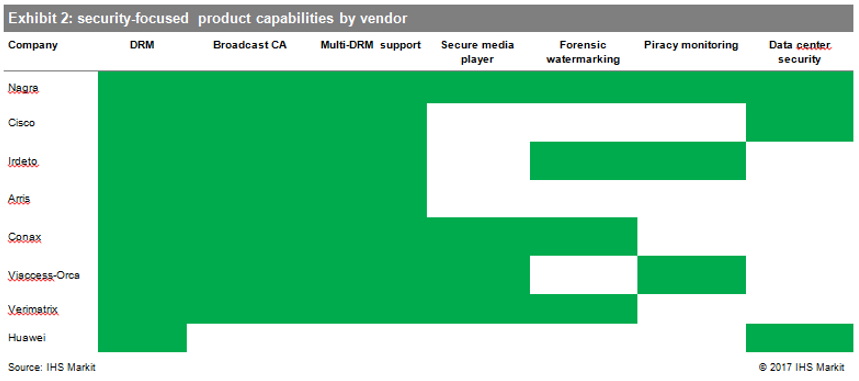

Broadcast CA and proprietary DRM are part-and-parcel of any minimum viable security solution, but encryption alone is no longer sufficient to impede illicit, systemic re-streaming. Secure media players, forensic watermarking, piracy monitoring, and infrastructure security form the crux of an expanded, holistic approach to revenue security.

“Media companies are not foolhardy, and they’re not prepared to predicate the integrity of their business model on passive encryption alone,” Kingston added. “Although the competitive landscape can shift quickly, at the present time NAGRA alone offers an end-to-end suite comprising transmission, storage, data center, and on-device security, as well as proprietary content tracking and proactive, piracy monitoring and takedown services. The company’s breadth of security offerings is currently unrivalled.”

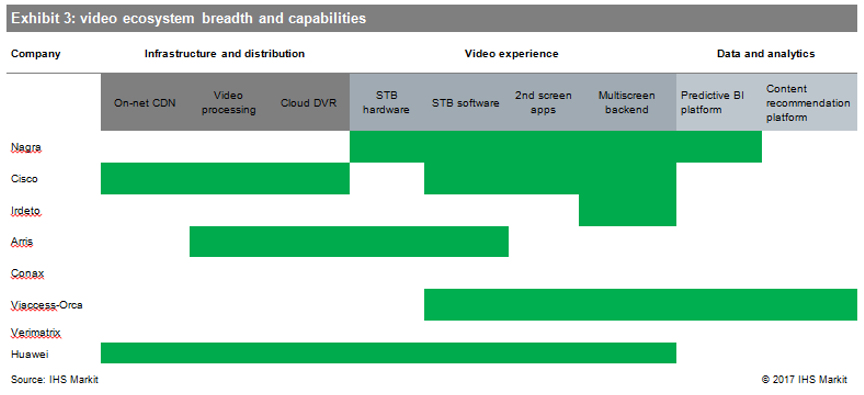

Competitive positioning in the wider technology ecosystem is far less clear-cut

Security forms only part of the broader technology ecosystem that media companies and service providers require. This broader video ecosystem draws together firms with expertise in infrastructure, video processing, video experience solutions, and analytics.

“From an R&D perspective, tailoring spend to achieve even a modicum of product specialization is a best-response for any firm in this industry. There exist only so many pivots that firm can feasibly or cost-effectively execute,” Kingston continued. “Moving into the network infrastructure space is a non-starter; the cost of entry, coupled with the hyper-competitive ARRIS-Cisco-Huawei oligopoly, precludes this form of diversification. However, firms with a provenance in video hardware, software, and apps have other diversification options at their disposal. The media industry is marching inexorably toward the ‘datafication’ of video operations. Among companies with a content security and video software background, few have established a competitive foothold in the analytics and predictive business-intelligence segment. Considerable first-mover advantage exists for those firms who secure an early foothold in this market.”

Latest News

- Barb to start reporting TV-set viewing of YouTube channels

- SAT FILM selects multi-DRM from CryptoGuard

- Qvest and ARABSAT to launch OTT streaming platform

- ArabyAds & LG Ad Solutions partner with TVekstra in Turkey

- Freeview NZ satellite TV service to move to Koreasat 6

- Comscore expands YouTube CTV measurement internationally