Dataxis reports on fixed satellite communication market

Wednesday, December 15th, 2021

State of Fixed Satellite Communication Market 2021

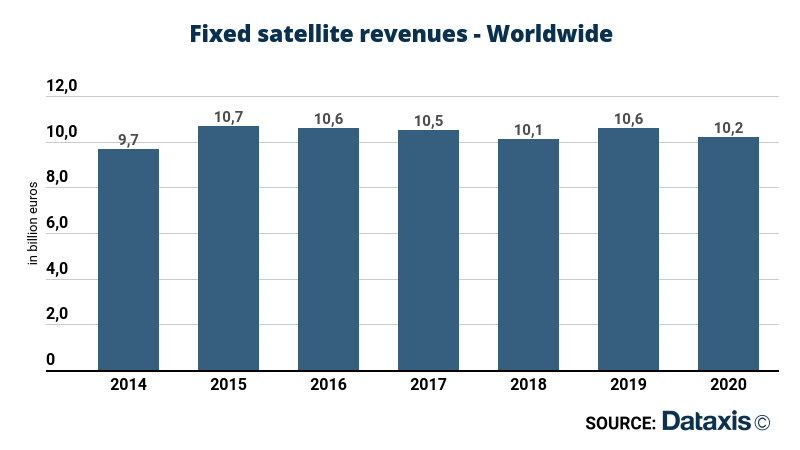

Dataxis has recently published its report on the Fixed Satellite Services (FSS) civil communications market. After years of significant growth, the decline in traditional video activity in the most developed countries is being sustained, resulting in a limited but steady decline in the turnover of FSS operators. The outlook for the future is equally becoming more pronounced.

Among the 45 civil communications satellite operators worldwide, the main players remain SES, Intelsat and Eutelsat. As regards to the operators’ fleet, a steady decline in new satellite launches can be noted. This naturally impinges on leading satellite platform providers worldwide: while in the course of 2018, 18 satellites were launched, the number decreased to 13 in 2019 and 9 in 2020. This market remains dominated by the Franco-German Airbus Space and the Franco-Italian Thales Alenia Space. In the launcher market, the French company Arianespace has maintained a prominent position, although it is facing growing competition from SpaceX. However, since control of space technologies is also a sovereignty issue, several countries, like Turkey with Turkish Aerospace, have developed their own offers to satisfy national demand on top of existing projects from China (CALT) or India (Antrix).

Dataxis observes that the growth of the FSS market increasingly depends on the development of adapted broadband offers, whether to satisfy retail or backhaul needs. Ka-band capacity is therefore significantly growing for most operators, particularly Eutelsat and Viasat. This approach, however, is being challenged by low or medium-orbit satellite constellation projects, the most emblematic being SpaceX’s Starlink. SpaceX’s revolution with cheaper and reusable launchers has changed the outlook when it comes to launching several hundred or thousands of satellites swiftly. In addition to Amazon’s Kuiper projects, there are initiatives linked to incumbent FSS operators, such as Telesat’s Lightspeed, 03B Networks (SES) and Oneweb, in which Eutelsat is also a shareholder.

It appears likely that historical FSS operators will not be sidelined in the constellation market in the coming years.

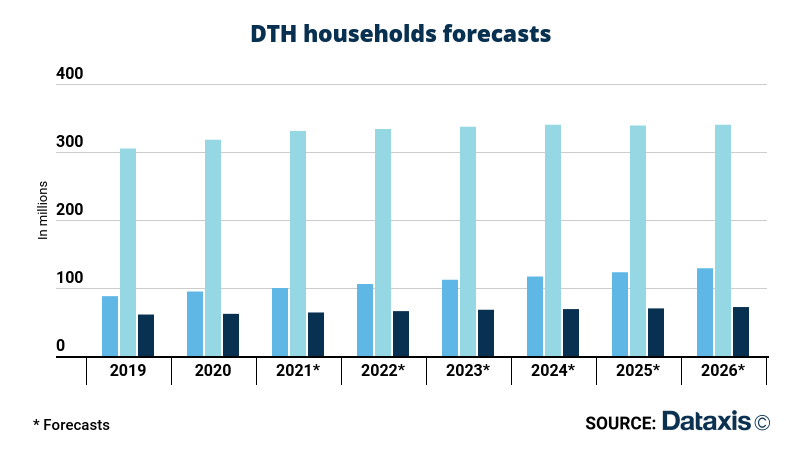

Dataxis has also issued its 2026 forecasts for the global satellite TV markets. It appears fairly obvious that some geographical areas are still very appealing for satellite video, most particularly Africa and MENA, as well as Asia-Pacific.

As far as one of the growth drivers is concerned, namely broadband, Dataxis reckons that this market will be relatively marginal in Western countries as a replacement or alternative to wireline or mobile offers. Nevertheless, although volumes are limited compared to fiber or 4G/5G, there is still significant growth potential for satellite operators. The capacity available can be filled by a relatively small number of internet subscribers. Additionally, the total number of satellite internet subscribers is relatively small according to Dataxis’ data and can be further expanded with offers that are more in line with current needs.

A significant part of the forthcoming growth of civil satellite operators will stem from the maritime and aviation sectors. The need for seamless broadband connectivity now extends to all locations and situations. In the maritime and aviation industries, fixed and mobile operators do not provide adequate solutions, making satellite operators, both FSS and constellation, ideally positioned. The recent acquisition of Inmarsat by Viasat is a striking example of this situation.

Latest News

- Barb to start reporting TV-set viewing of YouTube channels

- SAT FILM selects multi-DRM from CryptoGuard

- Qvest and ARABSAT to launch OTT streaming platform

- ArabyAds & LG Ad Solutions partner with TVekstra in Turkey

- Freeview NZ satellite TV service to move to Koreasat 6

- Comscore expands YouTube CTV measurement internationally